DC systems around the world have expanded significantly in recent years. It now represents the primary pension model in many markets and forms 63% of all pension assets in the top seven global pension markets.[1] This shift has increased the importance of how DC organisations govern investments, support members and design retirement pathways.

Thinking Ahead’s 2025 DC Peer Study shows an industry that is making changes in key areas, such as governance, investment strategy, operations and member support, while recognising that further development is needed to deliver stronger retirement outcomes.

Across interviews, survey responses and peer discussions with 20 DC organisations globally representing over $2tn of influential capital, a consistent message emerged: DC organisations are strongly committed to serving members, improving systems and raising standards, with the system is still evolving.

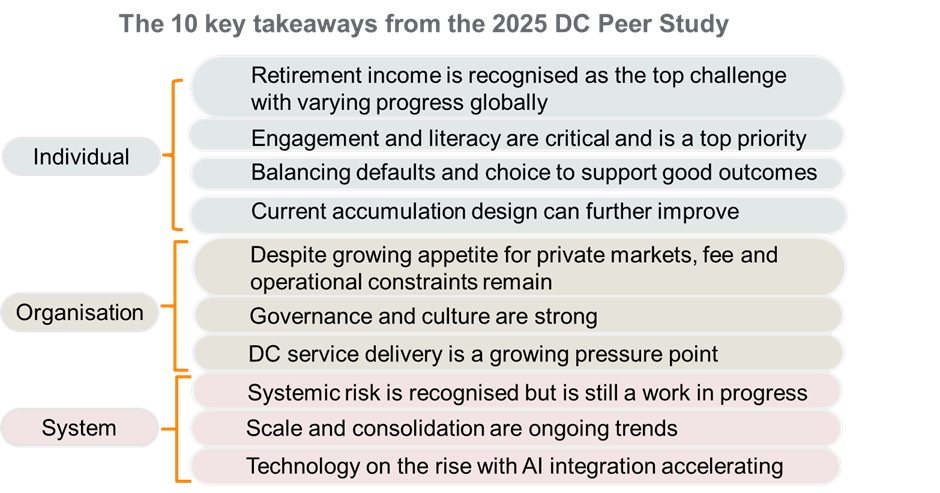

The ten takeaways from the study below capture the breadth of issues shaping DC systems today – from member behaviour and scheme design to operational pressures, governance and emerging technologies.

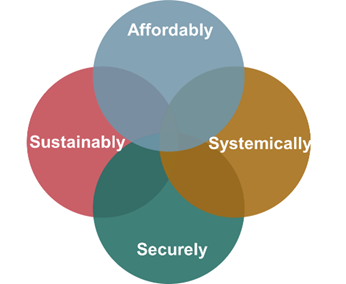

At the Thinking Ahead Institute, we believe any pension system must rest on four core design elements: security, affordability, sustainability across generations and systemic resilience over time.

Securely is positioned at the bottom of the framework and focuses on the security in outcomes.

Affordably relates to returns, so it sits at the top of the framework in the DC value proposition.

Sustainably is about fairness between generations, highlighting financial robustness over the long term.

Systemically refers to resilience across connected systems, focusing on the stability of the wider ecosystem.

These elements are interconnected and are often in tension with each other. Effective system design therefore requires balancing trade‑offs, navigating complexity and building resilience that can endure. The findings from the peer study illustrate the real‑world tensions DC organisations are having to work through.

Many DC organisations recognise that a complete member journey is better enabled by thoughtful support across both the accumulation and decumulation stages. While investment approaches during the saving phase have become more sophisticated, retirement income solutions remain varied across regions, with many systems still better designed for building balances than for converting savings into sustainable income.

Peer participants emphasised their responsibility to act in members’ interests through clearer communication, improved digital tools and more structured decision support. Member engagement remains a challenge in many markets, there is a noticeable shift toward designing simpler experiences and more targeted communications. Many organisations emphasised the importance of strengthening default pathways while still enabling meaningful choice. Advances in technology are expected to help support members in making informed choices.

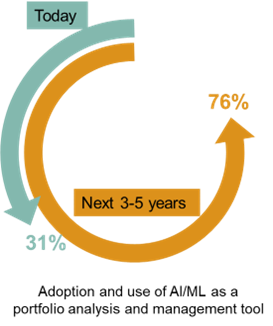

Technology is an area where change is accelerating. Most funds expect to increase spending on technology over the next five years. Organisations are investing in better data systems, digital member tools, automation and more efficient processes. AI is beginning to play a role, mainly in helping with data analysis, reporting, communication support and operational tasks. While many organisations remain cautious, the direction of travel is clear: technology will continue to support a more personalised service, stronger governance and improved operational resilience.

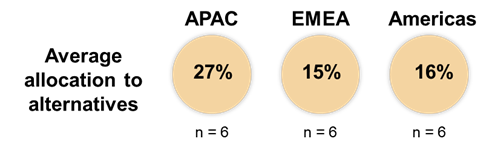

Peers noted that cost-sensitive operating models limit the ability to invest in more complex strategies, digital enhancements and private markets. While many organisations see private markets as an important source of diversification and returns, adoption remains uneven.

Larger funds are better able to integrate illiquid assets due to their scale and operational capacity, while others face barriers such as fees, liquidity requirements, governance and platform readiness. Despite these constraints, innovation in DC continues, with organisations exploring private markets, more personalised investment approaches and new retirement pathway designs to improve long-term member outcomes.

The team at Thinking Ahead has assessed the current state of DC using a red/amber/green scale. It shows that today’s DC system still operates with gaps across all four design elements, but there are clear opportunities to move towards a fit‑for‑future model. Providers can better support members by designing for income, not just drawdown, improving transparency on value for money, and raising service standards through better data, digital tools and benchmarking. There is also a need to define sustainability more clearly, track long‑term outcomes, and embed system resilience into decision‑making. Finally, reducing fragmentation and improving portability, data standards and policy alignment would strengthen the system and support better retirement outcomes.

Overall, this peer study reflects a DC sector that is evolving. The systems are getting bigger. The stakes are getting higher. And the need for a truly integrated, end‑to‑end pension experience, one that supports people not just in saving, but in living well after they stop working, has never been more urgent.

Building on the insights from the peer study, Thinking Ahead Institute’s 2026 DC priorities will focus on progressing work in retirement income, exploring greater use of private markets and more personalised member experiences.

Footnotes:

- Global Pension Assets Study 2026, Thinking Ahead Institute